HOME > BLOG > Finance > Financial Accounting Vs Managerial Accounting: Key Differences, Career Paths, and Skills

Finance

Financial Accounting Vs Managerial Accounting: Key Differences, Career Paths, and Skills

J

By Arif Siddiqui

April 16, 20256 min read

Last updated on April 21, 2026

SHARE THIS ARTICLE

Table Of Content

Understanding the Accounting Landscape

Financial Accounting Vs Managerial Accounting: Key Differences

Core Responsibilities in Financial Accounting Roles

Core Responsibilities in Managerial Accounting Roles

Finance and business professionals often reach a stage in their careers where they must understand the difference between reporting financial performance and using financial insights to guide business decisions. This distinction lies at the core of financial accounting and managerial accounting.

Professionals with expertise in financial accounting are in high demand in industries such as consulting, finance, and banking, particularly in fintech companies. According to salary data from AmbitionBox, Glassdoor, and Payscale (2024), for India, the average salary for entry-level jobs in financial accounting ranges from 3 to 6 LPA, whereas for mid-level jobs, it ranges from 8 to 18 LPA.

Understanding the Accounting Landscape

Financial accounting is used by organisations to ensure transparency and regulatory compliance, whereas managerial accounting is used by internal business teams to make business decisions.

Understanding the difference between financial accounting and managerial accounting will help finance and business professionals choose their career paths and gain expertise in their respective fields to adapt to the dynamic finance and business landscape.

Both branches focus on financial data but serve different audiences and purposes within a business ecosystem.

What is Financial Accounting?

*tickertape.in

Financial accounting focuses on recording, summarising, and reporting an organisation’s financial transactions to external stakeholders. These reports follow standardised frameworks such as IFRS or GAAP.

Key objectives include:

Preparing financial statements

Maintaining regulatory compliance

Ensuring transparency for investors and stakeholders

Tracking organisational financial health

Professionals specialising in financial accounting typically handle balance sheets, profit-and-loss statements, and cash-flow reports used by regulators, shareholders, and financial institutions.

What is Managerial Accounting?

*tickertape.in

While financial accounting addresses external reporting, managerial accounting focuses on internal decision-making.

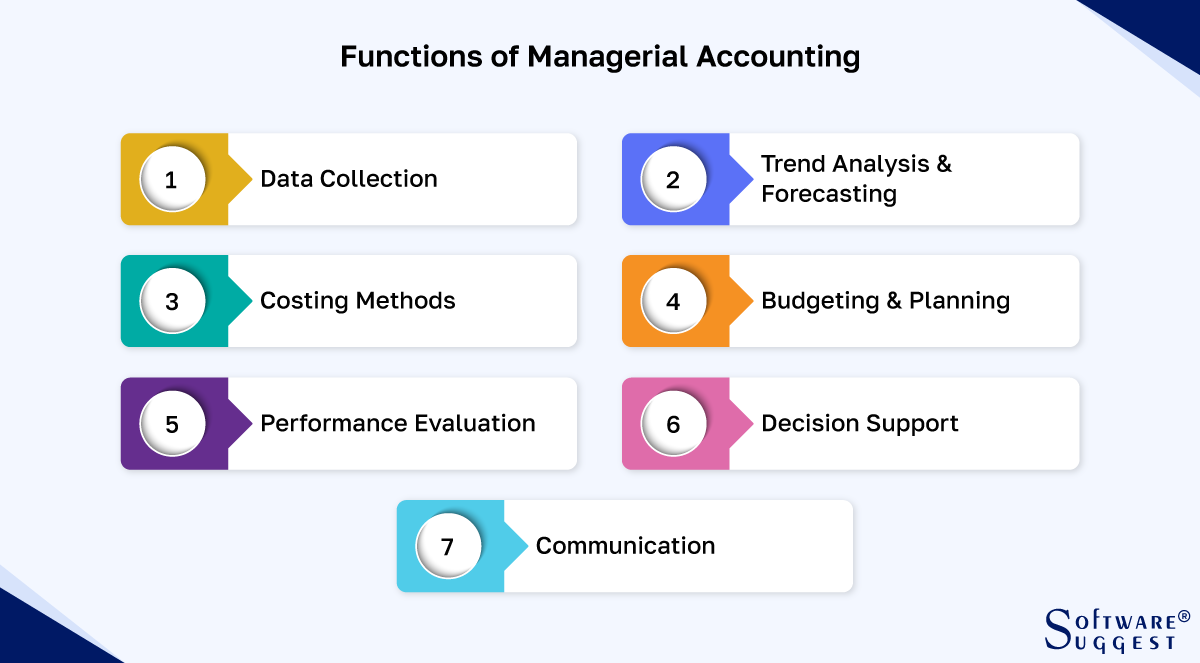

Managerial accounting provides insights that help management:

Plan budgets

Analyse operational performance

Forecast future financial scenarios

Optimise resource allocation

Unlike financial accounting, managerial accounting reports are not publicly disclosed and may vary across organisations based on internal requirements.

Financial Accounting Vs Managerial Accounting: Key Differences

Understanding the distinctions between the two fields helps professionals decide where their interests and career goals align.

Parameter

Financial Accounting

Managerial Accounting

Primary Purpose

External financial reporting

Internal decision-making

Audience

Investors, regulators, stakeholders

Managers and leadership

Reporting Standards

Must follow GAAP or IFRS

Flexible, organisation-specific

Reporting Frequency

Quarterly or annually

As required by management

Focus

Historical financial performance

Future planning and strategy

Confidentiality

Public disclosures

Internal use only

While financial accounting emphasises compliance and transparency, managerial accounting focuses more on performance insights and operational efficiency.

Core Responsibilities in Financial Accounting Roles

Professionals specialising in financial accounting typically perform the following functions:

Preparing financial statements

Recording and verifying transactions

Managing audits and regulatory filings

Ensuring compliance with accounting standards

Monitoring organisational financial performance

Strong analytical skills and attention to detail are essential because financial accounting requires precision in reporting and strict adherence to regulatory frameworks.

Core Responsibilities in Managerial Accounting Roles

Although closely related to financial accounting, managerial accounting responsibilities are more strategic. Typical functions include:

Budget planning and cost analysis

Profitability analysis

Financial forecasting

Operational performance evaluation

Strategic financial planning

Because managerial accounting works alongside business leadership, professionals often collaborate with operations, marketing, and strategy teams.

Career Opportunities in Financial Accounting

A career in financial accounting offers opportunities across industries such as consulting, banking, manufacturing, and technology.

These roles require expertise in financial accounting principles, financial reporting systems, and compliance standards. Professionals with certifications like Chartered Accountant, CMA, CPA, or specialised finance programmes often gain stronger career progression opportunities within financial accounting domains.

Professionals entering financial accounting roles benefit from developing both technical and analytical competencies.

Technical Skills

Financial statement preparation

Accounting standards (GAAP / IFRS)

Taxation fundamentals

Auditing procedures

Financial reporting tools

Analytical Skills

Data interpretation

Risk analysis

Regulatory compliance awareness

Financial forecasting basics

With increasing digital transformation in finance departments, professionals working in financial accounting are also expected to understand enterprise software such as SAP, Oracle Financials, and advanced spreadsheet modelling.

Free Course Recommendation: Build Foundations in Accounting

A beginner-friendly course designed for students, professionals, and entrepreneurs who want to understand the fundamentals of finance and how financial decisions influence business outcomes.

Practical insights from industry expert Ms. Vidhi Shah, Group Head of Finance at Tata Power (13+ years of experience across Deloitte and EY)

Free online certification upon completion

This course from Jaro Education offers a strong starting point for learners interested in building foundational knowledge before exploring advanced roles in financial accounting and finance.

Advantages and Challenges of Financial Accounting Careers

Careers in financial accounting offer strong professional stability and opportunities across industries. However, like most specialised fields, they also involve certain challenges related to regulatory compliance, accuracy, and reporting timelines.

Tight reporting deadlines during financial closing cycles

Despite these challenges, financial accounting continues to be a foundational pillar of corporate finance operations worldwide.

How Jaro Education Helps Professionals Advance in Finance

Upskilling plays a crucial role for professionals aiming to grow within financial accounting and related finance roles. Jaro Education acts as a trusted career guidance platform connecting learners with industry-relevant executive programmes and advanced certifications from reputed institutions.

Regulatory frameworks applicable to banks and NBFCs

Exposure to FinTech, analytics, and digital banking innovation

Marketing strategies used by banks and financial institutions

Industry-focused learning through case studies, group assignments, simulations, and term papers

This programme helps professionals strengthen industry knowledge while building expertise relevant to roles in banking, finance, and financial accounting.

Why Choose Jaro Education?

Jaro supports learners beyond course enrolment by offering:

Personalised counselling: Helping professionals choose programmes aligned with their career goals

Industry-aligned programme access: Courses designed based on evolving market insights

Jaro Connect ecosystem: A network for mentorship, career resources, and peer learning

For professionals looking to strengthen their expertise in financial accounting and expand into leadership roles, guided programme selection can significantly enhance long-term career prospects.

Choosing between financial accounting and managerial accounting ultimately depends on career aspirations and professional strengths. While financial accounting focuses on compliance, reporting, and transparency for external stakeholders, managerial accounting supports business and internal strategy decision-making. Both domains play crucial roles in modern organisations and offer rewarding career paths across industries.

For professionals aiming to build long-term careers in finance, the right mix of practical experience, advanced education, and industry exposure is essential. With personalised counselling, curated programmes, and access to leading academic institutions, Jaro Education helps professionals explore learning opportunities that align with evolving market demands. Taking the next step in professional development today can open doors to stronger expertise, leadership opportunities, and long-term career growth in finance.

Frequently Asked Questions

Jaro Education provides personalised counselling, academic guidance, and access to the Jaro Connect ecosystem, which offers networking opportunities, industry insights, and learning resources throughout the programme journey.

Yes. Most programmes offered through Jaro Education are designed for working professionals and are delivered through flexible online or blended learning formats, allowing learners to balance work and education.

Programmes offered through Jaro Education are developed in collaboration with reputed universities and institutes. They typically include structured curricula, expert faculty sessions, case studies, and industry-relevant learning outcomes.

Many professionals pursue finance programmes to strengthen expertise, develop strategic financial skills, and explore new opportunities within finance or business leadership roles.

No. Jaro Education acts as a service partner that provides counselling, learner support, and access to programmes offered by recognised universities or institutes. The degree or certification is granted by the respective academic institution.

Arif Siddiqui

Head of Accounting and Treasury

Arif Siddiqui is a finance leader specializing in accounting, treasury, and financial strategy. As Head of Finance at Generali Employee Benefits, he brings extensive experience in managing global financial operations. He is known for driving financial efficiency and governance across organizations. His leadership supports sustainable business growth and financial excellence.

Admission Closed

Admission Closed Admission Closed

Admission Closed Admission Open

Admission Open Admission Open

Admission Open